June 24, 2024 in Advisory Notes

Mould in Buildings and HVAC Systems

Mould plays an important role in the natural environment as a break-down mechanism for dead organic matter. In the built environment, it is an unwante...

March 2, 2023

Why is “Net-Zero” a Key Aspiration?

The 2015 Paris Agreement saw 196 countries, including Australia, commit to limit global warming to well below 2°C, and ideally to 1.5°C, compared to pre-industrial levels. Following this, the Intergovernmental Panel on Climate Change (IPCC) released their Special Report on the impacts of global warming of 1.5°C (“SR1.5”) in 2018. This report highlighted that the global economy needed to achieve net-zero carbon dioxide (CO2) emissions by around 2050 to have the best chance of meeting this 1.5°C target.

It was at this point that the setting of net-zero targets gained strong momentum across organisations and governments around the world.

What are the Key Drivers to set a Net-Zero Target?

As organisations develop and refine their Environmental, Social and Governance (ESG) frameworks to guide their actions through this decade, they are increasingly seeking to align the environmental impact of their operations with the global 1.5°C-aligned strategy to target net-zero emissions.

Beyond action on climate change, there are also material benefits to be gained by the target-setting organisation itself. These could include operational cost savings through energy efficiency activities; reducing supply-chain risk; unlocking competitive advantages; improved stakeholder relations and customer loyalty; and increased employee engagement.

It is now commonplace to see some form of net-zero emissions target included within any robust ESG strategy.

What Exactly Does Net-Zero Mean?

The term net-zero is used in reference to greenhouse gas (GHG) emissions, i.e. “net-zero emissions” or “net-zero GHG emissions”.

In practice, “emissions” here typically applies to the 7 GHG categories covered under the Kyoto Protocol, which include carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O) and hydrofluorocarbons (HFCs). If the term net-zero carbon or net-zero CO2 emissions is used, this generally refers to accounting for CO2 emissions only.

Net-zero GHG emissions in a global sense will occur when the global economy reaches a balancing point between the amount of GHG emissions human activity is putting into the atmosphere (“anthropogenic GHG emissions”) and the amount that human activity is removing from the atmosphere.

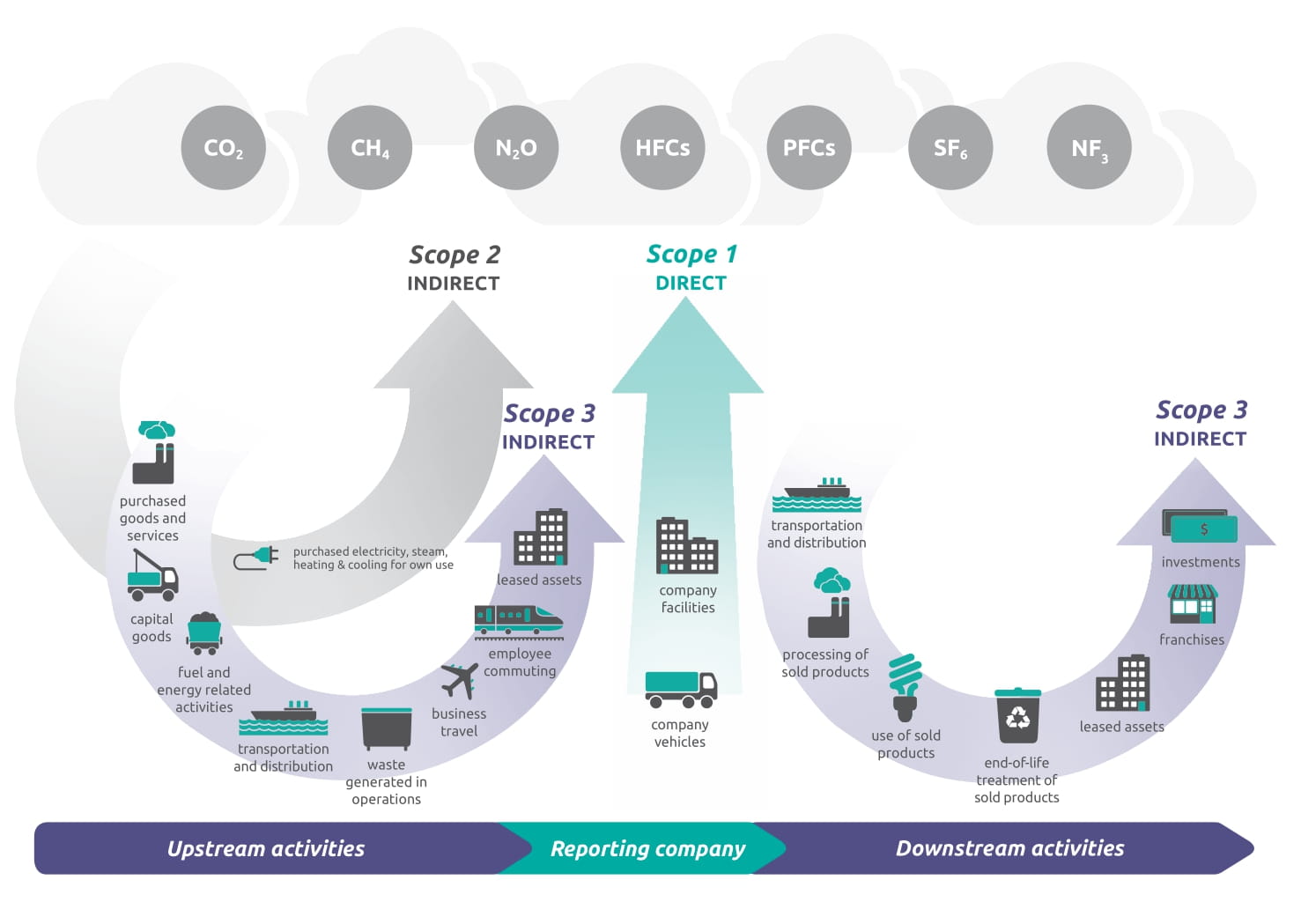

What are Scope 1, 2 and 3 Emissions?

GHG emissions are released to the atmosphere through a range of processes. These may include stationary combustion emissions from fossil fuel usage in boilers or generators; mobile combustion emissions from internal combustion engine vehicles; fugitive emissions from equipment leaks (e.g. refrigerant leaking from air-conditioning equipment); or process emissions from physical or chemical processing.

To assist in GHG emissions accounting across organisations, emissions from any of the sources described above are classified into 3 “Scopes”:

Scope 1 emissions occur from sources owned or controlled by the reporting organisation. Therefore, any stationary combustion emissions from company-owned natural-gas boilers, mobile combustion emissions from company-owned vehicles or fugitive refrigerant emissions from company-owned chillers would be classified as Scope 1 emissions for that company. Scope 1 emissions are relatively easy to quantify, and can be directly influenced by the reporting organisation. Any robust net-zero strategy must include Scope 1 emissions within their target boundary (an explanation of target boundaries is provided in the following section).

Scope 2 emissions are those associated with the generation of energy, typically electricity, which is purchased by the reporting organisation for their own use. These emissions physically occurred at the facility where the electricity was originally generated (such as a coal-powered power station), but form part of the Scope 2 emissions for the reporting organisation.

Like Scope 1 emissions, Scope 2 emissions are also relatively easy to quantify and directly influence, and therefore are virtually always included within a net-zero target boundary.

Scope 3 emissions are all emissions not included in Scope 1 or 2 that occur in the value chain of the reporting company, where “value chain” refers to all upstream and downstream activities associated with the operations of the reporting company. Scope 3 emissions typically account for the largest share of a company’s overall GHG emissions; however, they are also generally the most difficult to accurately quantify, or to directly influence solely by the reporting organisation. As a result, it is relatively common in the current market to see Scope 3 emissions excluded from a company’s stated net-zero target boundary; however, scrutiny over such omissions is likely to increase as we approach 2030.

The full Scope 1, 2 and 3 GHG emissions account for an organisation is defined as their GHG Emissions Inventory according to the GHG Protocol Standard, although in public discourse it is often referred to as the organisation’s “carbon footprint”.

More information on GHG Protocol Standards can be found at https://ghgprotocol.org/standards

How Do Net-Zero Targets Differ?

The Science Based Targets initiative (SBTi – https://sciencebasedtargets.org/ ) provides a helpful framework for understanding the key elements within an organisation’s stated net-zero target:

How Does an Organisation Become Certified Net-Zero?

At the time of writing, there is no uniformly accepted standard or framework for certification of net-zero status, either in Australia or internationally; however, there are certain frameworks that are broadly adopted.

Whilst adhering to such a framework or gaining certification for net-zero target setting is not currently subject to Australian legislation, doing so provides a strong signal to the market that your organisation has a robust strategy in place that has been independently reviewed by a reputable third-party certifier, and may therefore be less susceptible to being perceived as a form of “greenwashing”.

One of the most relevant net-zero frameworks applicable to organisations operating within the Australian property sector is Climate Active. More information can be found at: https://www.climateactive.org.au/

Internationally there are a number of relevant net-zero frameworks:

What are the Implications for your Organisation and Facilities?

Typical actions to align with net-zero emissions operations are best described by addressing each emissions scope.

Addressing Scope 1 Emissions

Addressing Scope 2 Emissions

Addressing Scope 3 Emissions

The GHG Protocol Scope 3 standard defines 15 categories of Scope 3 emissions, further sub-categorised as “upstream” or “downstream” emissions, depending on where they occur in an organisation’s value chain.

Scope 3 emissions vary greatly based on market sector and geographic location and as such, the activities required to address them are similarly varied. A foundational step in this process is accurately accounting for, and reporting on, the full range of Scope 3 emissions that an organisation is responsible for under their target boundary.

Examples of Scope 3 emissions relevant to buildings or organisations within the property sector are:

.

For more information on Net Zero facilities contact:

Andrew Nagarajah, A.G. Coombs Advisory

T: +61 3 9248 2700 | E: anagarajah@agcoombs.com.au

The A.G. Coombs Group has committed to a Net Zero goal: Scope 1 and Scope 2 operational emissions by 2030, is working with its value chain, industry partners and customers to achieve Net Zero Scope 3 emissions by 2040.

For more information on A.G. Coombs Net Zero 2030 commitment, go to: https://www.agcoombs.com.au/news-and-publications/news/a-g-coombs-group-net-zero-2030/

.

.

.

.

download pdf

June 24, 2024 in Advisory Notes

Mould plays an important role in the natural environment as a break-down mechanism for dead organic matter. In the built environment, it is an unwante...

April 30, 2024 in Advisory Notes

A lot has changed since A.G. Coombs released our first Advisory Note on heat pumps back in 2018. Increasingly, asset owners are no longer asking if he...

March 12, 2024 in Advisory Notes

Building owners and facility managers often don’t have access to a full set of accurate documentation for of their buildings to support effective an...

October 4, 2023 in Advisory Notes

As the construction and property sectors continue to develop and embrace new technologies including digital twins, cognitive buildings, artificial int...